But the 1099 path in sales isn't just about filing different tax forms. It involves a distinct legal status, self-managed taxes, contract negotiations that can make or break your income, and the discipline to run what is essentially your own sales business. This guide walks through exactly what that looks like — from the IRS definitions that determine your classification to the steps for getting set up and getting paid.

Key Takeaways

- A 1099 sales rep is legally self-employed — no taxes are withheld, and you pay self-employment tax plus income tax yourself

- Setup requires choosing a business structure, getting an EIN, opening a business bank account, and signing a solid contractor agreement

- Quarterly estimated tax payments are required; budget 25–30% of income for taxes (verify current rates at IRS.gov)

- Compensation typically comes through commission-only or draw-against-commission structures — each with different cash flow implications

- Top reps frequently out-earn W-2 peers — but the model rewards financial discipline and consistent pipeline management

What Is a 1099 Independent Contractor Sales Rep?

A 1099 sales rep is a self-employed professional who sells products or services on behalf of one or more companies and receives a Form 1099-NEC (Nonemployee Compensation) instead of a W-2. The hiring company does not withhold taxes, pay benefits, or contribute to Social Security and Medicare on the rep's behalf.

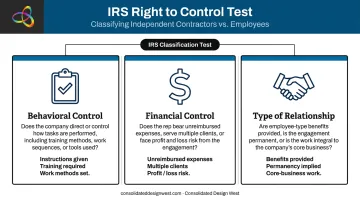

The IRS "Right to Control" Test

The legal line between employee and contractor comes down to control. According to the IRS, the key distinction is this: a company can direct what result a worker achieves, but if it also controls how the work gets done — the schedule, methods, and tools — that's an employee relationship.

The IRS evaluates three categories:

- Behavioral control — Does the company direct how tasks are performed, or just the outcome?

- Financial control — Does the rep have unreimbursed expenses, work for multiple clients, and risk profit or loss?

- Type of relationship — Are there employee-type benefits, a permanent arrangement, or is the work integral to the company's core business?

Misclassification carries real consequences for both sides. The IRS can hold a company liable for unpaid employment taxes, and the worker loses out because the employer's share was never paid — meaning your retirement and Social Security credits take the hit too.

1099 vs. W-2 Sales Reps

Knowing where you fall on that spectrum shapes everything from your tax obligations to your earning ceiling. Here's how the two arrangements compare:

| Factor | W-2 Sales Rep | 1099 Sales Rep |

|---|---|---|

| Tax withholding | Employer handles it | You handle it |

| Benefits | Employer-provided | Self-funded |

| Commission rates | Generally lower | Generally higher |

| Multiple clients | Typically restricted | Common arrangement |

| Schedule control | Set by employer | Self-determined |

W-2 roles offer predictability. 1099 roles trade that predictability for higher commission rates and the freedom to work with multiple clients — but that trade only works if you're set up to manage the self-employment side correctly.

Step-by-Step: How to Set Up as a 1099 Sales Rep

Becoming a 1099 sales rep requires two parallel tracks: administrative setup (legal and financial) and commercial setup (building your sales business). Skipping either one creates problems down the road.

Step 1: Choose and Register Your Business Structure

Your three main options:

- Sole proprietorship — Simplest to start, but offers zero liability protection. Your personal assets are exposed if something goes wrong.

- LLC — The most common choice for independent sales reps. Separates personal and business liability, and is relatively straightforward to set up at the state level through your state's SBA registration process.

- S-Corporation — Used when income is high enough to justify tax optimization through salary/distribution splitting. There's no universal threshold, and the IRS focuses on reasonable compensation requirements rather than a dollar figure.

Most new 1099 sales reps start with an LLC. Consult a CPA or business attorney before choosing — the right structure depends on your income level, state, and liability exposure.

Step 2: Obtain an EIN and Open a Business Bank Account

An Employer Identification Number (EIN) functions as your business's Social Security number. The IRS issues EINs for free, and the online application issues one immediately upon approval.

You'll need the EIN to:

- Open a dedicated business bank account

- Provide to companies issuing you a Form 1099-NEC

- File business taxes accurately

Keeping business and personal finances completely separate isn't optional — it's how you protect personal assets, track income accurately, and avoid an accounting nightmare at tax time.

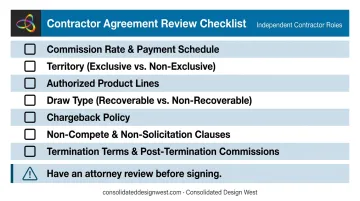

Step 3: Understand and Sign Your Contractor Agreement

A contractor agreement is where most 1099 sales reps get burned. Before signing anything, verify the contract clearly defines:

- Commission rate and payment schedule

- Sales territory and whether it's exclusive or non-exclusive

- Product lines you're authorized to represent

- Whether a draw is offered — and whether it's recoverable or non-recoverable

- Chargeback policy (what happens if a deal reverses after commission is paid)

- Non-compete and non-solicitation clauses

- Termination terms and what happens to earned commissions after termination

Have an attorney review the agreement before you sign. A few hundred dollars in legal fees upfront can prevent costly contract disputes later.

Step 4: Set Up Your Tax and Invoicing Systems

From day one, track every dollar in and every business expense out. Accurate records keep your tax liability correct and your deductions defensible when it counts.

Essential setup:

- Accounting software (even basic tools work for most solo reps)

- A system for logging mileage from the first client meeting

- A folder for receipts and documentation on every business purchase

- A calendar reminder for quarterly estimated tax deadlines

IRS Form 1040-ES is used to calculate and submit estimated quarterly payments. Set it up before your first commission hits — not after.

Step 5: Build Your Principal Portfolio

Unlike a W-2 employee, a 1099 sales rep can represent multiple non-competing companies simultaneously. Each company you represent is called a "principal." Diversifying across principals protects your income if one relationship ends.

When evaluating a principal, look at:

- Commission structure and payment timing

- Product quality and brand reputation in the market

- What support they provide (leads, marketing materials, order processing)

- Contract fairness, especially territory and termination clauses

Consolidated Design West, an Anaheim, CA-based packaging and co-manufacturing solutions provider with over 34 years of experience, actively partners with independent 1099 sales reps to sell its B2B portfolio. Reps earn 60% of net profits per closed deal with no earnings cap, receive company-supplied warm leads, and have all order processing handled by CDW. When you're building your portfolio, look for principals that combine a strong commission rate with operational support — that combination is what makes a rep relationship worth committing to.

Taxes and Deductions for 1099 Sales Reps

Self-Employment Tax

According to IRS Topic 554, the self-employment tax rate is 15.3%, consisting of:

- 12.4% for Social Security

- 2.9% for Medicare

This covers both the employee and employer portions — which means you're paying what would normally be split between you and an employer. On top of that, you owe federal and state income tax. The total burden surprises many reps who only look at the commission rate when deciding whether to go 1099. One offset worth noting: the IRS allows you to deduct the employer-equivalent portion of self-employment tax when calculating your adjusted gross income.

Quarterly Estimated Taxes

Because no employer withholds taxes on your behalf, you're required to pay estimated taxes four times per year. The IRS schedule:

| Payment Period | Due Date |

|---|---|

| January 1 – March 31 | April 15 |

| April 1 – May 31 | June 15 |

| June 1 – August 31 | September 15 |

| September 1 – December 31 | January 15 (following year) |

Missing or underpaying these estimates triggers an IRS penalty. The practical fix: set aside a fixed percentage of every commission payment the moment it hits your account — before you spend any of it.

The $600 Rule for Form 1099-NEC

Any company that pays you $600 or more in a calendar year must issue a Form 1099-NEC. Note: the IRS has indicated a higher threshold of $2,000 applies to payments made after December 31, 2025 — verify current requirements at IRS.gov before filing. Regardless of whether you receive a 1099 form, you're required to report all income to the IRS.

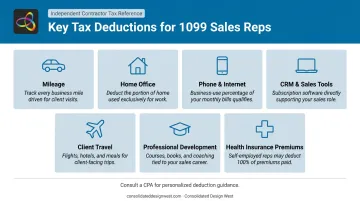

Key Deductions for Sales Reps

These deductions can meaningfully reduce your taxable income:

- Mileage — The IRS standard rate is 70 cents per mile for business use (verify current rate at IRS.gov before filing)

- Home office — Deductible if you use a dedicated space exclusively and regularly for business

- Phone and internet — The business-use portion may be deductible

- CRM software and sales tools — Ordinary and necessary business expenses

- Travel for client meetings — Transportation, lodging, and business meals (verify current meal deductibility rules)

- Professional development — Courses, certifications, industry memberships

- Health insurance premiums — Self-employed individuals can deduct these via Form 7206

A CPA who works regularly with self-employed sales reps can identify deductions you'd likely miss on your own — particularly around home office allocation, mileage logs, and mixed-use expenses like phone and internet. The fee is typically deductible as a business expense.

Compensation Structures for 1099 Sales Reps

Commission-Only

The most common structure: you earn a percentage of each sale, nothing more. Rates are higher than W-2 equivalents to account for the absence of salary, benefits, and employer tax contributions. Key variables that determine where your rate lands:

- Industry margin and average deal size

- Sales cycle length and complexity

- Territory size and account density

- Whether the principal provides leads or you source your own

Draw Against Commission

A draw is a regular advance payment — weekly or monthly — against future commissions you haven't yet earned. Two structures exist:

- Recoverable draw — The advance must be repaid if earned commissions don't cover it. You're borrowing against future production and carry the repayment obligation until commissions catch up.

- Non-recoverable draw — Functions as a guaranteed minimum floor. If commissions fall short, you keep the draw and owe nothing back.

That said, draws aren't standard across the board. Many manufacturers' rep arrangements — especially in B2B markets where commissions are paid after orders ship — are commission-only with no advance structure at all.

Territory and Exclusivity

Contractor agreements typically define a geographic territory or list of named accounts. Key distinctions:

- Exclusive territory — No other rep (employed or contracted) can sell in your territory

- Non-exclusive territory — You compete with direct reps or other contractors on the same accounts

Exclusivity directly affects income potential. If a principal sells into your territory through its own direct sales team or other reps, your commission opportunity is diluted. Negotiate for exclusive territory rights during the ramp period at minimum.

Negotiation Checklist Before Signing

Before agreeing to represent any principal:

- Research commission rates for comparable products in the same industry before any conversation begins

- Negotiate for a non-recoverable draw during the initial ramp period if offered

- Clarify the chargeback policy — what happens to paid commissions if a sale reverses

- Get territory exclusivity confirmed in writing, not just verbally agreed upon

- Understand termination terms, including how commissions on open orders are handled

Common Misconceptions About 1099 Sales Rep Work

"1099 Means I Don't Have to Pay Taxes"

The opposite is true — you pay more. As an independent contractor, you cover both the employee and employer portions of Social Security and Medicare. That's a 15.3% self-employment tax before income tax applies. Without proactive quarterly payments, expect a large year-end bill and potential IRS underpayment penalties.

"I Can Deduct Everything as a Business Expense"

Deductions must be ordinary and necessary — common in your trade and directly tied to your sales work. Personal expenses can't be reclassified as business costs, and poor documentation is a consistent audit trigger. Keep records for every deduction, every year.

"Higher Commission Rates Automatically Mean Higher Take-Home Pay"

The commission percentage is only one variable. Before comparing any offer to a W-2 salary, factor in:

- Self-employment tax (15.3%)

- Self-funded health insurance and retirement contributions

- Income variability between slow and strong months

- Operating costs: software, travel, phone

A 60% commission structure like the one Consolidated Design West offers can absolutely outpace a W-2 salary — but only if the net calculation accounts for all costs, not just the headline rate.

Frequently Asked Questions

What qualifies as an independent contractor?

The IRS uses a "right to control" test across three categories: behavioral control, financial control, and type of relationship. If the company directs only the result of your work — not how you do it — you're generally an independent contractor. All three categories are weighed together, not independently.

What taxes do you have to pay as a 1099 contractor?

You owe self-employment tax at 15.3% (12.4% Social Security + 2.9% Medicare), plus federal and state income tax. These are paid quarterly through estimated tax payments using IRS Form 1040-ES. An additional 0.9% Medicare tax applies above certain income thresholds.

What is the $600 rule for 1099?

Any business that pays you $600 or more in a calendar year must issue a Form 1099-NEC. Starting with payments made after December 31, 2025, the IRS threshold increases to $2,000 — verify current requirements at IRS.gov. You must report all income regardless of whether a 1099 is issued.

What can I write off as a 1099 salesperson?

Common deductions include mileage (70 cents per mile), home office, phone and internet (business portion), CRM software and sales tools, client travel, and self-employed health insurance premiums. Keep detailed records for everything and consult a tax professional for personalized guidance.

Is a 1099 sales job worth it?

For high-performing, self-motivated reps with strong closing skills, yes — the income ceiling is higher than most W-2 roles, but so is the variance. Financial discipline, proactive pipeline management, and a clear-eyed understanding of the tax burden are what separate successful 1099 reps from those who struggle.

What does a draw mean in sales?

A draw is a regular advance payment against future commissions that provides short-term income stability. A recoverable draw must be repaid if your commissions fall short of the advance. A non-recoverable draw functions as a guaranteed minimum — no repayment required if commissions don't cover it.