: Complete Template & Guide](https://file-host.link/website/consolidateddesignwest-86bidz/assets/blog-images/5d8d727e-1d15-4bbf-a3e6-683f39514037/1779891121338968_907b1e09640242648237add599aa051a/360.webp)

Without a properly drafted contract, the risks pile up fast: IRS misclassification audits, commission disputes, lost customer relationships, and back-tax liability that can reach well into five figures per violation.

This guide covers everything you need to build a defensible 1099 sales rep agreement — the required components, sales-specific clauses, tax obligations, and the misclassification red flags that can unravel even the best-intentioned contractor arrangement.

TL;DR: Key Takeaways

- A 1099 sales rep agreement defines the working relationship, compensation, territory, and obligations — without creating employer-employee status

- Every agreement needs: scope of work, commission terms, confidentiality, termination conditions, IP rights, and governing law

- Sales-specific clauses generic contracts miss: territory rights, exclusivity terms, commission disputes, and post-termination customer ownership

- Businesses paying a rep $600 or more in a calendar year must file IRS Form 1099-NEC by January 31

- Calling someone a contractor doesn't make them one — the actual working conditions must hold up under IRS and DOL scrutiny

What Is a 1099 Independent Contractor Agreement for Sales Reps?

A 1099 independent contractor agreement for sales reps is a legally binding contract between a business and a self-employed sales professional. It confirms that the rep is not an employee, will be paid and reported on IRS Form 1099-NEC, and is responsible for their own taxes and benefits.

How Sales Rep Agreements Differ from Generic IC Contracts

A standard freelancer contract covers basic scope and payment. A sales rep agreement handles more ground — sales reps generate revenue directly, often work on commission, may represent multiple companies at once, and operate within defined territories. A generic independent contractor agreement doesn't cover that exposure.

Sales-specific issues requiring explicit contract language include:

- Commission calculation and payment triggers

- Territory rights and exclusivity

- What happens to commission on deals in progress at termination

- Who owns the customer relationships after the agreement ends

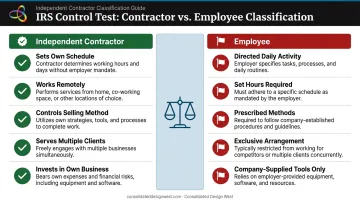

The IRS Control Test

According to IRS Topic 762, the core question for contractor classification is whether the company controls only the result of the work — the closed sale — not the method — how the rep goes about selling. For sales relationships, this distinction is nuanced. Some direction is expected and acceptable; controlling daily activity is not.

CDW's rep structure is a practical example: the company provides warm leads and handles order processing, but reps set their own schedules, work remotely, and operate with full autonomy over how they sell. Any well-drafted sales rep agreement should make that autonomy explicit — both to satisfy the IRS control test and to set clear expectations from day one.

Key Components: What Your Sales Rep 1099 Agreement Must Include

Party Identification and Effective Date

The agreement opens by naming both parties using their full legal names, listing addresses, and establishing an effective date. This sets jurisdiction, identifies who is bound by the terms, and anchors any dispute resolution.

Scope of Work and Sales Responsibilities

This section defines what the rep is authorized to sell, which customer types or industries they serve, and what falls outside their scope. Vague scope language is the most common source of commission disputes. For reps selling CDW's packaging components and co-manufacturing services across multiple verticals, precision here matters. Be specific about:

- Which product lines or service categories are included

- Which customer segments the rep is authorized to target

- Whether there are any accounts the rep cannot pursue (house accounts)

- Required activity levels, if any (demos, outreach cadence)

Compensation Terms

This is the section most likely to generate conflict if it's ambiguous. It must specify:

- Whether pay is commission-only, a draw against commission, or a flat project fee

- The exact commission percentage or dollar amount per closed deal

- When commission is earned — at contract signing, invoice payment, or deposit receipt

- Payment timing — Net 15 or Net 30 are standard for contractor invoicing

CDW's reps earn 60% of net profits per closed deal with no cap and no base — a pure commission-only structure. Whatever your arrangement, the agreement must define "net profit" explicitly. Leaving that term undefined is an open invitation to disputes.

Termination Conditions

The agreement should specify:

- Whether either party can terminate at will

- How much advance notice is required (30 days is common)

- How commissions on in-progress deals are handled at termination

- Whether the rep is owed commission on deals that close after their last day

A rep who spent months building a deal shouldn't lose that commission without clear contractual language — and the company shouldn't face open-ended payment obligations without a defined cutoff period.

Confidentiality, Governing Law, and Dispute Resolution

These three clauses round out the agreement's legal foundation:

- Confidentiality — Protects pricing, client lists, and product strategies from competitors; must survive termination and continue applying after the agreement ends

- Governing law — Specifies which state's law controls; critical for companies with reps operating across multiple states

- Dispute resolution — Establishes whether disputes go through arbitration before litigation, which is faster and less expensive than going straight to court

Sales-Rep-Specific Clauses You Can't Skip

Generic IC agreements leave out the provisions that matter most in sales relationships — the ones that determine who owns the customer, who gets credit for a deal, and whether a rep can even sign the agreement without risking misclassification. These four clauses require precise language.

Territory Rights

A territory clause defines where the rep is authorized to sell — by geography, vertical market, or both. It must also state whether the territory is:

- Exclusive: the company won't sell directly or use other reps in that territory

- Non-exclusive: other reps or direct sales efforts may operate in the same space

Exclusivity is a major negotiating point, especially for reps who cover broad geographic regions. Spell out the terms explicitly — vague territory language leads directly to conflicts over commission credit.

Product and Client Exclusivity

Can the rep represent competing vendors simultaneously? This is a defining issue for independent sales professionals, many of whom build their business by representing multiple non-competing lines.

If exclusivity is required, the agreement should document what the company provides in return — a higher commission rate, a protected territory, or a guaranteed minimum pipeline. Experienced reps will push back on exclusivity unless the agreement offers measurable compensation in return. Beyond negotiation, under the DOL's economic reality test, requiring a rep to work exclusively for one company strengthens the argument that they're actually an employee.

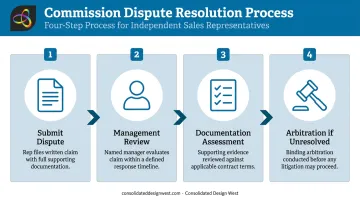

Commission Dispute Resolution

What happens when two reps claim credit for the same deal? What if a client cancels an order after commission was already paid? The agreement needs a defined process:

- Who reviews the dispute (a named manager or role)

- What documentation is required to support a claim

- The timeline for resolution

- Whether unresolved disputes go to arbitration

Without this process in writing, a disputed $15,000 commission can stall for months — and often ends in court.

Post-Termination Customer Ownership and Non-Solicitation

After the agreement ends, who owns the customer relationships — the company or the rep? Most agreements assign ownership to the company, with a non-solicitation period of 12–24 months preventing the rep from targeting those clients directly.

Two important distinctions:

- Non-solicitation: the rep can't actively pursue former clients, but can still work in the industry

- Non-compete: the rep can't work in the industry at all — courts scrutinize these heavily, and several states effectively prohibit them

Keep post-termination restrictions narrow and specific. Overly broad language gets struck down in litigation, leaving the company with no protection at all.

1099 Tax Obligations: What Both Parties Need to Know

The $600 Threshold and Form 1099-NEC

IRS Form 1099-NEC applies when a business pays an independent contractor $600 or more in a calendar year. The form must be provided to the contractor and filed with the IRS by January 31 of the following year. Businesses filing 10 or more information returns are required to e-file.

Collecting Form W-9

Get a completed W-9 from every rep before work begins. The W-9 provides the rep's Taxpayer Identification Number, which is required for 1099-NEC reporting. Missing a valid TIN triggers mandatory backup withholding at 24% on all reportable payments — a compliance issue that a single onboarding step eliminates.

Self-Employment Tax and Quarterly Payments

Unlike W-2 employees, 1099 sales reps pay both sides of Social Security and Medicare. For 2026, the self-employment tax rate is 15.3% — 12.4% Social Security and 2.9% Medicare — on net self-employment earnings. The Social Security portion applies on earnings up to $184,500.

Reps must make quarterly estimated tax payments using Form 1040-ES if they expect to owe at least $1,000 in taxes after withholding. Commission-only reps with variable income should set aside roughly 25–30% of each commission check to cover both SE tax and income tax obligations.

What Sales Reps Can Deduct

Independent contractor reps can deduct ordinary and necessary business expenses. Common deductions include:

- Vehicle mileage at the IRS 2026 rate of 72.5 cents per mile for client visits and territory travel

- Home office costs (must be used regularly and exclusively for business)

- Phone and internet used for business

- Marketing materials, samples, and professional subscriptions

- Professional development and industry conferences

The IRS requires documentation for all deductions. Mileage logs must record date, destination, and business purpose for each trip — treat this as a non-negotiable habit.

Worker Misclassification: How to Stay on the Right Side of the IRS

The IRS Three-Category Test

The IRS evaluates classification across three categories:

| Category | What It Examines | Sales Rep Red Flag |

|---|---|---|

| Behavioral control | Does the company direct how work is performed? | Required scripts, mandatory call schedules, prescribed routes |

| Financial control | Does the company control the business aspects of the job? | Regular wage-like payments regardless of sales, no rep investment in their own business |

| Type of relationship | Written contracts, benefits, and permanency | Indefinite exclusive arrangement functioning like an internal sales department |

No single factor is decisive. The IRS looks at the totality of the relationship.

The DOL's Economic Reality Test

The DOL's 2024 rule, effective March 11, 2024, asks whether a worker is genuinely in business for themselves or economically dependent on one company. Enforcement was paused in May 2025 while the DOL reconsiders the rule, but the underlying analysis still shapes how auditors think.

For sales reps, the highest-risk scenario is an indefinite, exclusive, single-principal arrangement — no independent business investments, no other clients, and full reliance on one company's lead pipeline. That profile draws serious scrutiny.

What Labeling Someone a Contractor Won't Fix

Calling someone a contractor in the agreement doesn't make them one. Behaviors that signal an employer-employee relationship include:

- Setting the rep's working hours

- Requiring exclusive use of company systems

- Prohibiting the rep from working with other clients

- Micromanaging the sales process

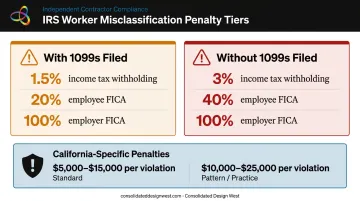

Misclassification penalties are steep. With 1099s filed, IRS Section 3509 liability can reach 1.5% income tax withholding plus 20% of employee FICA plus all employer FICA. Without required 1099s filed, those rates jump to 3% and 40% respectively. In California specifically, willful misclassification carries penalties of $5,000–$15,000 per violation, rising to $10,000–$25,000 per violation for a pattern or practice.

When in doubt, consult a labor attorney — especially if your reps work exclusively for your company, receive company-supplied leads, or follow any standardized selling process.

Frequently Asked Questions

What is a 1099 independent contractor agreement?

It's a legal contract between a business and a self-employed worker that defines the scope of work, payment terms, and confirms non-employee status. The business reports payments on IRS Form 1099-NEC rather than a W-2, and the worker handles their own taxes and benefits.

Can a salesperson be an independent contractor?

Yes — as long as the company controls the result (the closed sale) but not the method or schedule. A properly drafted 1099 sales rep agreement documents this distinction and helps protect the classification if it's ever challenged.

Do I have to file a 1099 form for an independent contractor?

Yes. Businesses must file IRS Form 1099-NEC for any contractor paid $600 or more in a tax year. The form is due to both the contractor and the IRS by January 31 of the following year.

What are the four requirements of a valid enforceable contract?

A valid contract requires four elements: offer, acceptance, consideration (services exchanged for payment), and mutual assent (both parties agree willingly, without fraud or coercion). All four must be present for the agreement to be legally enforceable.

What can independent contractors write off 100%?

Sales reps can generally deduct 100% of ordinary and necessary business expenses: home office costs, business-related phone and internet, professional subscriptions, and marketing materials. Rules vary by situation, so consult a tax professional to confirm what applies to your circumstances.