The real question is what each arrangement actually pays after the IRS takes its share. That calculation is more complicated than most reps realize, and the answer changes depending on your income level, your state, and how many legitimate business expenses you can deduct.

This article breaks down exactly how each arrangement is taxed, what deductions are available to each, and which structure tends to produce higher take-home pay — with the math to back it up.

Key Takeaways

- 1099 sales reps pay the full 15.3% self-employment tax (both employee and employer sides of FICA), but can deduct business expenses W2 reps generally cannot

- W2 reps pay only 7.65% employee FICA since employers cover the other half

- Employer-provided benefits add roughly 30% on top of wages, per BLS data

- At the same gross income, 1099 reps typically owe more in taxes, but higher commission rates and available deductions can close or reverse that gap

- The 1099 advantage grows with income; W2 benefits matter most at lower income levels

- Run the numbers on your actual rate, deductions, and benefits before choosing a structure

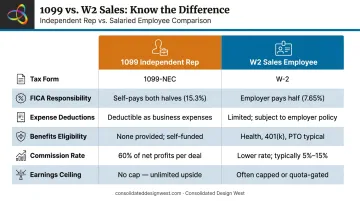

1099 vs W2 for Sales Reps: Quick Comparison

| Factor | 1099 Independent Rep | W2 Sales Employee |

|---|---|---|

| Tax form issued | Form 1099-NEC | Form W2 |

| Who pays FICA | Rep pays full 15.3% | Split: 7.65% employee, 7.65% employer |

| Tax collection method | Quarterly estimated payments | Withheld from each paycheck |

| Business expense deductions | Yes — broad deduction access | No — suspended through 2025 by TCJA |

| Benefits eligibility | No employer benefits | Health insurance, 401(k), PTO |

| Commission structure | Typically higher rates | Typically lower rates |

| Earnings ceiling | Uncapped | Often capped or quota-linked |

The Classification Issue

The IRS determines worker status by asking one central question: does the company control how the work gets done, or just the outcome? If it controls both the result and the methods, the worker is an employee. If it controls only the result, the worker is an independent contractor. The IRS evaluates this through three lenses — behavioral control, financial control, and the overall type of relationship.

This classification isn't a choice either party makes freely. It must reflect the actual working relationship — equipment ownership, scheduling autonomy, exclusivity, and control over methods all factor in. Misclassifying an employee as a contractor carries real IRS penalties, including back taxes and potential liability under Section 3509.

Starting in 2020, companies report contractor commissions on Form 1099-NEC (not 1099-MISC). The issuing company files the form; the rep is responsible for reporting the income and paying their own taxes.

How the 1099 Tax Burden Works for Sales Reps

Self-Employment Tax: The Big Number

When you're a 1099 contractor, you're both the employee and the employer in the eyes of the IRS. That means you pay the full 15.3% self-employment tax: 12.4% Social Security (up to the $184,500 wage base in 2026) plus 2.9% Medicare with no cap.

There's a partial offset: you can deduct half of your self-employment tax from gross income before calculating your income tax. On $100,000 in net profit, the math looks like this:

- SE tax: ~$14,130

- Deductible half: ~$7,065

- Adjusted gross income reduced by $7,065 before income tax is calculated

You can also deduct self-employed health insurance premiums directly from gross income, which further reduces the bite. Neither deduction eliminates the SE tax burden, but they're meaningful.

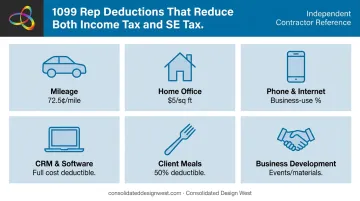

Business Expense Deductions

This is where 1099 reps gain real ground. Deductible expenses reduce your net profit before SE tax is even calculated — meaning every legitimate deduction saves you both income tax and self-employment tax.

Key deductions for sales reps:

- Mileage — 72.5 cents per mile for 2026, or actual vehicle expenses

- Home office — $5 per square foot (simplified method, up to 300 sq ft), for space used regularly and exclusively for business

- Phone and internet — business-use percentage of your actual bills

- CRM and sales software subscriptions — ordinary and necessary business tools

- Client meals — 50% deductible when you're present and the meal has a clear business purpose

- Business development costs — marketing materials, professional memberships, trade events

A rep with $18,000 in legitimate deductions on $100,000 in gross earnings only pays SE tax on $82,000 — roughly $2,165 less in SE tax alone.

Quarterly Estimated Taxes

1099 reps must pay taxes four times a year: April 15, June 15, September 15, and January 15. If you expect to owe $1,000 or more after withholding and credits, you're generally required to make these payments or face underpayment penalties.

Setting aside 25–30% of gross earnings is the standard recommendation to cover federal income tax, self-employment tax, and state tax. The exact percentage varies by state and total deductions. Treat it as a cash flow discipline — not an afterthought.

Who the 1099 Model Fits

The 1099 structure tends to work best for:

- Experienced reps with an existing book of business or client network

- Reps representing multiple product lines who have real, documentable business expenses

- High earners who can leverage deductions to meaningfully reduce taxable net income

- Reps in no-income-tax states (Texas, Florida, Nevada) where the 1099 math improves further

That last point matters more than most reps realize. A rep closing deals in Texas or Florida on a 60% commission structure — like the model Consolidated Design West uses for its independent contractor sales force — nets more than a W2 rep in California or New York earning the same gross, simply because the state tax bill doesn't exist. The 1099 structure rewards that kind of intentional setup.

How W2 Taxation Works for Sales Reps

The FICA Advantage

W2 employees pay only 7.65% employee FICA — 6.2% Social Security plus 1.45% Medicare. The employer matches every dollar, covering the other half of the total 15.3% FICA bill. On $100,000 in W2 compensation, you save roughly $7,065 in FICA compared to the same income as a 1099 rep.

Federal and state income taxes are withheld automatically from each paycheck. If your withholding doesn't match your actual liability (common for commission-heavy W2 roles with variable pay), you can adjust your W4 at any time to request more or less withholding.

Benefits: The Hidden Compensation

W2 compensation isn't just salary. According to the Bureau of Labor Statistics ECEC data for December 2025, benefits averaged $13.79 per hour for private-industry workers — roughly 29.9% of total employer compensation costs.

A W2 sales rep earning $75,000 in cash compensation might be receiving total compensation closer to $100,000. Employer health insurance contributions, 401(k) matching, paid time off, and workers' compensation all add up — none of it appears on your offer letter, but it directly affects what the role is actually worth.

The Deduction Gap

Since the Tax Cuts and Jobs Act of 2017, W2 employees cannot deduct unreimbursed job expenses on federal returns for tax years 2018 through 2025. That includes:

- Mileage and vehicle use

- Phone and internet costs

- CRM subscriptions and sales tools

- Home office expenses

The standard deduction ($15,750 for single filers in 2025) is your primary lever. Itemizing is allowed for mortgage interest, charitable donations, and medical expenses — but job-related sales costs are off the table. If your employer doesn't reimburse these expenses, you absorb them out of after-tax income.

When W2 Works Better

The W2 structure tends to make more sense when:

- You're new to an industry and need training, onboarding, and a runway to build pipeline

- Employer-subsidized health insurance is a significant value (easily $8,000–$20,000+ annually)

- Your legitimate business deductions would be minimal

- You need predictable income while establishing yourself

Which Pays More After Taxes? Running the Numbers

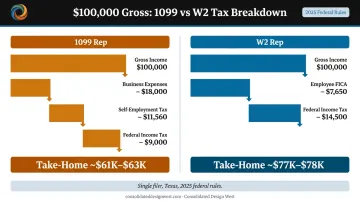

A $100,000 Gross Comparison

The following figures are approximations using 2025 federal tax rules for a single filer in Texas (no state income tax). Consult a CPA before making decisions based on these numbers.

1099 Rep — $100,000 gross commissions:

- Deduct $18,000 in business expenses → $82,000 net profit

- SE tax (15.3%): ~$11,560 (half deductible: ~$5,780)

- AGI: ~$76,220

- Standard deduction: $15,750 → taxable income ~$60,470

- Estimated federal income tax: ~$9,000

- Estimated take-home: ~$61,000–$63,000

W2 Rep — $100,000 gross compensation:

- Employee FICA (7.65%): ~$7,650

- Standard deduction: $15,750 → taxable income ~$84,250

- Estimated federal income tax: ~$14,500

- Estimated take-home: ~$77,000–$78,000 (cash only)

At the same gross income with no state tax, the W2 rep takes home more cash. But the raw numbers miss the two variables that actually determine who comes out ahead.

The Commission Rate Premium

1099 companies typically offer higher commission rates because they're not paying employer FICA, benefits, HR overhead, or equipment costs. A W2 rep earning 5% commission on $1M in sales earns $50,000 gross. A 1099 rep earning 8% on the same deals earns $80,000 gross — a $30,000 difference before taxes enter the picture.

The rate differential isn't arbitrary: companies pass saved employer costs back through higher commission rates. That structural shift is what makes the gross-income comparison move so sharply in the 1099 rep's favor.

The Break-Even Dynamic

At lower income levels, W2 benefits — especially health insurance — often outweigh the 1099 commission advantage. Above $150,000, deduction leverage and the commission premium start to dominate. The crossover point depends on:

- Your W2 benefits package value (health, dental, 401k match)

- Your actual deductible business expenses

- Your state's income tax rate

- The size of the commission rate differential

Geography compounds this — a 1099 rep in Texas pays no state income tax, while the same rep in California hits a 9.3% marginal state rate around $100,000 in taxable income. 1099 reps working across state lines may also face multi-state filing obligations based on where clients receive the benefit of services.

When to Choose 1099 vs W2 as a Sales Rep

The right structure depends on where you are in your career and what you need from your income right now.

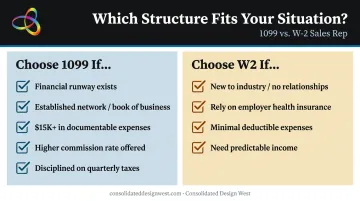

Choose 1099 if:

- You have 3–6 months of financial runway before you need consistent income

- You have an existing network, territory, or book of business

- You can legitimately document $15,000+ in annual business expenses

- The commission rate is meaningfully higher than the equivalent W2 offer

- You're disciplined about quarterly tax payments and expense tracking

Choose W2 if:

- You're entering a new industry or sales motion without established relationships

- You rely on employer-subsidized health insurance

- Your potential deductions are minimal and wouldn't materially reduce your tax bill

- You value predictable income over maximum upside

The hybrid situation: Some sales reps hold a W2 position while also earning 1099 income from a separate independent arrangement. It creates a specific tax obligation: quarterly estimated payments must account for total income across both sources, and self-employment tax applies to the 1099 earnings regardless of your W2 withholding.

Frequently Asked Questions

Is it better to get paid with W-2 or 1099?

It depends on your income level, deductible expenses, and benefits needs. W2 offers employer-covered tax sharing and benefits stability; 1099 can produce higher after-tax income for experienced reps who can leverage deductions and negotiate higher commission rates. There's no universal answer.

Are salespeople 1099 or W-2?

Both are common. Inside sales and strategic account reps are typically W2 employees; independent sales agents, manufacturers' reps, and territory contractors are frequently 1099. The structure depends on the company, industry, and degree of control exercised over the rep's work methods.

Does W-2 get taxed more than 1099?

Not exactly. W2 reps pay less in self-employment tax because the employer covers half of FICA. But 1099 reps can offset their higher tax burden through business deductions. At the same gross income and before deductions, 1099 reps typically owe more total tax.

What business expenses can a 1099 sales rep deduct?

Key deductible expenses include mileage at the current IRS rate (70 cents/mile for 2025 — verify annually), home office space, phone and internet (business-use percentage), CRM and sales software, client meals (50%), and business development costs. These reduce taxable net income before self-employment tax is calculated.

Do 1099 sales reps need to pay taxes quarterly?

Yes. 1099 contractors must generally make estimated quarterly tax payments to the IRS — and to their state, if applicable — to avoid underpayment penalties. The standard due dates are April 15, June 15, September 15, and January 15.

Can a sales rep be both 1099 and W2 at the same time?

Yes. A rep can hold a W2 primary role and receive 1099 income from a separate independent sales arrangement at the same time. All income must be reported, self-employment taxes apply to the 1099 portion, and quarterly estimated payments should account for the combined liability from both sources.