Introduction

Short answer: yes. A 1099 contractor can legally work for multiple companies at the same time — and in many cases, doing so actually strengthens their classification as a genuine independent contractor under IRS guidelines.

That said, "legally permitted" and "completely unrestricted" aren't the same thing. Individual contracts may contain non-compete or exclusivity clauses that limit who a contractor can work for, regardless of what federal law allows.

The working arrangement itself matters too. When it starts to look more like employment — single client, set hours, company-controlled methods — misclassification becomes a real risk for both parties.

This guide breaks down how the IRS defines contractor status, the tax mechanics of receiving multiple 1099-NEC forms, what contract clauses can restrict multi-client work, and practical steps for managing it all cleanly.

Key Takeaways

- 1099 contractors can work for multiple companies simultaneously — a sign of genuine contractor status under IRS rules

- Each company paying $600+ in a calendar year must issue a separate 1099-NEC; contractors must report all income regardless of whether a form was issued

- Contract clauses — non-competes and exclusivity terms — can restrict multi-client work even when federal law allows it

- Exclusivity arrangements can blur the contractor/employee line in the IRS's view, regardless of how the contract labels the worker

What Makes Someone a 1099 Contractor?

A 1099 contractor (or independent contractor) is self-employed. No employer withholds taxes from their pay, they receive a 1099-NEC instead of a W-2 at tax time, and they're responsible for their own Social Security, Medicare, and income tax obligations.

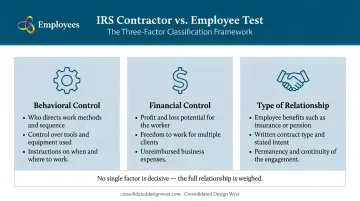

The IRS Three-Factor Test

IRS Topic 762 identifies three categories of facts used to determine whether a worker is truly independent:

- Behavioral control — Does the company direct how the work gets done, or only the result? Controlling methods, tools, and work sequence points toward employment.

- Financial control — Can the worker profit or lose money? Do they advertise services, work with multiple clients, and carry unreimbursed expenses? Business-like financial independence supports contractor status.

- Type of relationship — Are there employee-type benefits? A written contract? Is the work arrangement permanent or project-based?

No single factor is decisive. IRS Publication 1779 is explicit: the entire relationship must be weighed together.

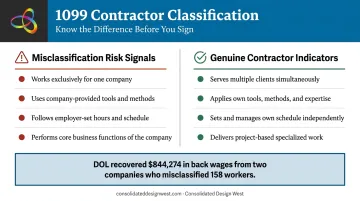

A 1099-NEC form or a contract labeled "independent contractor" doesn't automatically create contractor status. The IRS examines the actual working relationship — control, independence, and financial structure. Working for multiple clients is one of the clearest signals of genuine independence, because it shows the worker is running a business, not functioning as a de facto employee of a single company.

Can a 1099 Contractor Legally Work for Multiple Companies?

Yes. No federal law prevents it — and the IRS actively treats multi-client work as evidence of legitimate contractor status.

No IRS rule, DOL regulation, or federal statute prohibits a 1099 contractor from serving multiple clients simultaneously. In fact, the opposite is true: making services available to the market, advertising, and taking on multiple jobs are all cited in IRS and DOL guidance as indicators of legitimate independent contractor status.

Why Multi-Client Work Supports Contractor Classification

IRS Publication 15-A states that independent contractors are generally free to seek out business opportunities, advertise, maintain a visible business location, and offer services in the relevant market. The DOL's Fact Sheet 13 adds that sporadic or project-based work where a worker takes on multiple different jobs indicates independent contractor status.

The contrast matters: a W-2 employee typically works for one employer, follows that employer's methods, uses their tools, and operates on a set schedule. A contractor operates independently — setting their own hours, choosing their clients, and directing their own work methods.

That flexibility is exactly what makes the model common in B2B sales, marketing, logistics, and packaging. Consolidated Design West, for example, builds national sales coverage through 1099 reps who work remotely with full schedule autonomy — serving beauty, food and beverage, electronics, and pet care clients across the country.

Where Misclassification Risk Appears

The IRS draws a clear line. If a contractor:

- Works exclusively for one company over an extended period

- Uses that company's tools and follows its methods

- Works set hours at the company's direction

- Performs core business functions rather than specialized project work

...the arrangement starts to resemble employment, regardless of what the contract says. Both the contractor and the hiring company can face IRS penalties as a result. The DOL recovered $844,274 in back wages from just two Louisiana home care providers who misclassified 158 workers, demonstrating that enforcement carries real financial consequences for both parties.

Temporarily working with one client during a slow period won't disqualify contractor status on its own. What matters is whether the full relationship — across behavioral, financial, and relational factors — reflects genuine independence.

Tax Implications When Working with Multiple Companies

Multiple clients means multiple 1099-NEC forms — but the tax system treats all that income as a single pool of self-employment earnings, not separate categories per client.

How 1099-NEC Forms Work With Multiple Clients

Any company that pays a contractor $600 or more in a calendar year must issue a separate Form 1099-NEC. A contractor working with four companies may receive four forms. Crucially, Copy A of each form goes directly to the IRS — meaning the agency can match what companies report against what contractors declare.

All income must be reported, even if no form was issued (for payments under the threshold, or from clients who simply didn't file).

Self-Employment Tax

Because no employer withholds taxes on 1099 income, contractors pay self-employment tax on net earnings. IRS Publication 334 sets the current rate at 15.3% — made up of 12.4% Social Security and 2.9% Medicare. This applies to combined net self-employment earnings from all clients once they exceed $400.

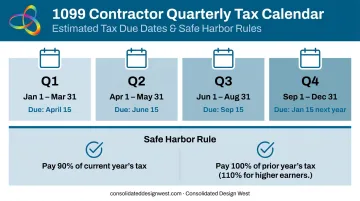

Quarterly Estimated Payments

Because that self-employment tax accumulates across all clients, contractors typically owe taxes throughout the year — not just at filing time. The IRS requires quarterly estimated payments on the following schedule:

| Payment Period | Due Date |

|---|---|

| January 1 – March 31 | April 15 |

| April 1 – May 31 | June 15 |

| June 1 – August 31 | September 15 |

| September 1 – December 31 | January 15 (following year) |

To avoid underpayment penalties, IRS Publication 505 recommends paying the smaller of 90% of the current year's tax or 100% of the prior year's tax (110% for higher-income filers).

Deductions and Recordkeeping

Business expenses used while serving multiple clients — home office, equipment, software, travel — may be deductible against self-employment income on Schedule C. A tax professional can help identify which expenses qualify and how to document them correctly.

Keeping records separated by client pays off in several ways:

- Simplifies tax filing when income sources vary by quarter

- Resolves payment disputes faster with clear per-client documentation

- Provides clean records if the IRS ever requests verification

What to Watch Out For: Non-Competes, Conflicts of Interest, and Contracts

The IRS permitting multi-client work and an individual contract permitting it are two separate things. Before taking on a new client, review every existing agreement carefully.

Non-Compete Clauses

Non-compete agreements can restrict a contractor from working with direct competitors for a defined geographic area and time period. These clauses appear frequently in sales representation agreements, consulting contracts, and product development roles.

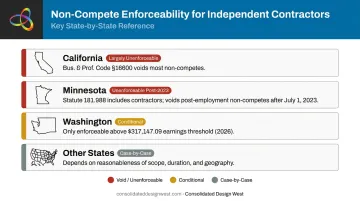

Enforceability varies significantly by state:

- California — Business and Professions Code Section 16600 voids most non-compete agreements broadly; it applies to "anyone," not just employees

- Minnesota — Statute 181.988 explicitly includes independent contractors and makes post-employment non-competes void for agreements entered after July 1, 2023

- Washington — Non-competes are only enforceable above an earnings threshold; the 2026 threshold for independent contractors is $317,147.09

- Most other states — Enforceability depends on reasonableness of scope, duration, and geographic limits

The FTC's 2024 rule that would have banned non-competes nationally was blocked by a federal court and is currently not enforceable. State law remains the controlling framework.

Conflict-of-Interest Provisions

Even without a formal non-compete, some contracts prohibit contractors from working with clients in the same industry or on overlapping projects where confidential information could be shared. These provisions can be broader than they appear. If the language feels ambiguous, get written legal clarification before you sign.

Exclusivity Arrangements

Some companies offer higher pay in exchange for exclusivity. Contractors should weigh this carefully. Beyond the earnings tradeoff, accepting exclusivity can itself become evidence of misclassification — IRS Publication 15-A treats lack of freedom to work other jobs as a factor pointing toward employee status.

When in doubt about any contract term, request clarification in writing and keep a copy. A paper trail protects you if a dispute arises later.

Practical Tips for 1099 Contractors Managing Multiple Clients

Managing multiple client relationships without friction comes down to two things: solid structure and proactive communication.

Business setup:

- Use separate invoices and payment records for each client

- Open a dedicated business bank account to keep personal and business finances distinct

- Consider forming an LLC to formalize your independent status and limit personal liability

Contract management:

- Before signing anything new, review all existing contracts for non-compete, exclusivity, or confidentiality clauses

- Get any ambiguous restrictions clarified in writing — don't assume

- Use clear project scopes and defined deliverable timelines in every client agreement

Day-to-day operations:

- Use scheduling tools to avoid commitment overlaps that could affect delivery quality

- Be transparent with clients that you run a multi-client practice — without disclosing confidential details from other relationships

- Track income and expenses by client throughout the year, not just at tax time

Contractors who apply these habits consistently find that managing five clients is no harder than managing two — the systems do the heavy lifting.

Frequently Asked Questions

Can you work two 1099 jobs at the same time?

Yes. There is no federal law or IRS rule preventing a contractor from holding multiple 1099 engagements simultaneously. The only restrictions that could apply are contractual — such as non-compete or exclusivity clauses in individual agreements.

Can you be a sales rep for multiple companies?

Yes. 1099 sales reps routinely represent multiple non-competing companies, carrying complementary product lines and serving overlapping territories across the same client base. It's one of the more practical arrangements the independent contractor model enables.

How many 1099-NEC forms can a contractor receive in one year?

There is no limit. A contractor receives one 1099-NEC from each company that paid them $600 or more during the calendar year. All income from all sources must be reported on the tax return, regardless of how many forms arrive.

Can a company require a 1099 contractor to work exclusively for them?

A company can request exclusivity through a contract clause, but contractors should be cautious. Exclusivity arrangements can signal misclassification under IRS criteria, and whether the clause is enforceable depends heavily on state law.

Does working for only one company make a 1099 contractor an employee?

Not automatically. Working with a single client during a given period doesn't determine status by itself. The IRS looks at the full picture — behavioral control, financial independence, and the nature of the relationship — not just client count.

What happens if I don't report income from all my 1099 clients?

All 1099 income must be reported regardless of whether a form was issued. Since companies file Copy A of each 1099-NEC directly with the IRS, unreported income is cross-referenced by the IRS. Penalties include a 0.5% monthly failure-to-pay penalty (up to 25% of unpaid taxes), a 20% accuracy-related penalty for negligence or substantial understatement, plus daily compounding interest at the current underpayment rate.