This guide covers exactly what a 1099-NEC is, when it's required, who's exempt, how the W-9 fits in, and what contractors should do once the form arrives. One important note on timing: the $600 threshold applies for 2025 reporting, but IRS Publication 1099 (2026) raises that threshold to $2,000 for tax years beginning after 2025.

Key Takeaways

- Businesses that paid a contractor $600 or more for services in 2025 must issue a Form 1099-NEC by January 31

- The $600 threshold is cumulative — multiple smaller payments throughout the year count toward the total

- Contractors must report all self-employment income on their tax return, even without a 1099

- C corps and S corps are generally exempt from receiving a 1099-NEC (attorneys are the key exception)

- The self-employment tax rate is 15.3% — contractors pay both the employee and employer share

What Is a 1099-NEC and Why Do Contractors Receive One?

A Form 1099-NEC (Nonemployee Compensation) is the IRS tax information form used to report payments made to independent contractors, freelancers, consultants, and other self-employed individuals. Think of it as the contractor counterpart to a W-2: a W-2 goes to employees and reports wages with taxes already withheld, while a 1099-NEC reports gross payments with nothing withheld.

A Brief History Worth Knowing

Before tax year 2020, nonemployee compensation was reported in Box 7 of Form 1099-MISC. The IRS reintroduced the standalone 1099-NEC form starting with 2020 returns. If you've seen older references to "1099-MISC for contractor payments," that's why.

Why the IRS Requires It

Because no taxes are withheld from contractor payments, the IRS uses 1099s as a cross-reference tool. When a business files a 1099-NEC, the IRS can verify that the contractor reported matching income on their return. The form documents what was paid — it doesn't determine what you owe.

Receiving a 1099 doesn't mean you owe taxes on the exact dollar amount shown. The form reports gross payments. Contractors still deduct legitimate business expenses from that figure and pay self-employment tax — currently 15.3% (12.4% Social Security + 2.9% Medicare) — on net earnings.

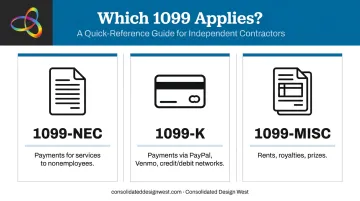

Other 1099 Forms You Might Encounter

| Form | When It Applies |

|---|---|

| 1099-NEC | Payments for services from a business to a nonemployee |

| 1099-K | Payments via credit card, PayPal, Venmo (business), or other third-party networks |

| 1099-MISC | Rents, royalties, prizes, and other miscellaneous income categories |

If a business paid you through PayPal or a similar platform, they won't issue a 1099-NEC — the payment processor files a 1099-K instead.

When Is a Business Required to Issue a 1099 to a Contractor?

Any business that pays an independent contractor $600 or more for services during the tax year must issue a Form 1099-NEC. This applies to services only — not goods or materials purchased from a vendor.

The $600 Threshold Explained

The threshold is cumulative across the full calendar year, not per invoice. Three payments of $200, $250, and $200 total $650 — that triggers the 1099 requirement. IRS instructions for Form 1099-NEC confirm this applies to fees, commissions, and prizes paid for services performed by a nonemployee.

A few important clarifications:

- Payments under $600 are still taxable income for the contractor — they just don't trigger the business's filing obligation

- The $600 threshold applies to services, not merchandise or supplies

- Starting with tax years after 2025, the threshold increases to $2,000, with inflation adjustments beginning in 2027

For businesses working with multiple contractors — sales reps, marketing consultants, freelance designers — tracking cumulative payments throughout the year (not just in January) prevents last-minute scrambles.

Filing Deadlines and Penalties

Both deadlines fall on January 31:

- Copy B must be sent to the contractor by January 31

- Copy A must be filed with the IRS by January 31 (paper or electronic)

- Businesses with 10 or more information returns must e-file via the IRS IRIS or FIRE systems

Missing these deadlines gets expensive. Per the IRS information return penalties page, the 2026 penalty tiers are:

| How Late | Per-Return Penalty |

|---|---|

| Up to 30 days late | $60 |

| 31 days late through August 1 | $130 |

| After August 1 or not filed | $340 |

| Intentional disregard | $680 minimum — no cap |

For small businesses (average annual gross receipts of $5 million or less), reduced maximums apply — but the per-return amounts are the same. A handful of missed 1099s adds up fast.

Who Is NOT Required to Receive a 1099-NEC?

Not every contractor triggers a 1099 obligation. Several exemptions apply depending on entity type, payment method, and the nature of the transaction.

Corporate entities:

- Contractors operating as C corporations or S corporations generally do not receive a 1099-NEC

- Exception: Payments to attorneys require a 1099-NEC regardless of corporate structure — attorney fees are always reportable

Payment method:

- If payment was made via credit card, debit card, PayPal, Venmo (business accounts), or other third-party payment networks, the business does not issue a 1099-NEC. The payment processor handles a 1099-K instead. This trips up a lot of businesses.

Other exceptions:

- Payments made for personal, non-business purposes

- Payments to foreign contractors — these may require Form 1042-S instead

- Payments for merchandise or goods only (with no service component)

The W-9 form the contractor submits tells you their entity type, so collect it before the first payment to avoid guessing later.

The W-9: The Step That Comes Before the 1099

Before issuing a 1099, a business must collect a completed Form W-9 from the contractor. The W-9 captures:

- Legal name and address

- Taxpayer Identification Number (SSN or EIN)

- Entity type (sole proprietor, LLC, S corp, C corp, etc.)

The entity type determines whether a 1099-NEC is required at all. This is why the W-9 should be collected before the first payment — not at year-end.

Who Does What

A common point of confusion: the contractor fills out the W-9, not the 1099. The W-9 stays with the hiring business. The business uses that information to prepare the 1099-NEC at year-end. The contractor never sees or touches the 1099-NEC until the business sends Copy B in January.

Best Practices for Businesses

- Collect the W-9 during contractor onboarding — before the first payment clears, not scrambling at year-end

- Validate name/TIN combinations using the IRS TIN Matching Program, a free IRS tool that catches mismatches before they trigger a filing penalty

- Keep W-9s on file for at least four years per IRS recordkeeping guidelines — you'll need them if a return is ever questioned

These steps matter at any scale. For Consolidated Design West, which brings on 1099 commission-only sales representatives across the US, getting W-9s signed at onboarding means accurate year-end reporting for the company and no surprises for the rep come January.

What Contractors Should Do When They Receive a 1099-NEC

Reading the Form

The 1099-NEC is straightforward. Look for:

- Box 1 — Nonemployee compensation (the total paid to you for the year)

- Payer's name and TIN

- Your name and TIN

Box 1 is the number you'll work from when filing.

Where It Goes on Your Tax Return

Contractors report self-employment income on Schedule C (Profit or Loss from Business), which feeds into Form 1040. The 1099-NEC itself isn't "filed" — it's a reference document. You report the income; the IRS cross-references it against what the payer reported. Schedule SE then calculates your self-employment tax obligation.

Verifying Accuracy

Compare Box 1 against your own payment records. If the numbers don't match:

- Contact the payer first — request a corrected 1099-NEC

- If a corrected form isn't issued in time, still report the correct income amount based on your records and note the discrepancy

Self-Employment Tax and Estimated Payments

Because no taxes are withheld from contractor pay, you're responsible for both the employee and employer portions of Social Security and Medicare: the full 15.3% on net self-employment earnings.

The good news: you can deduct half of self-employment tax when calculating adjusted gross income.

To avoid underpayment penalties, make quarterly estimated tax payments using Form 1040-ES. The 2026 due dates are April 15, June 15, September 15, and January 15 (2027).

The IRS safe harbor thresholds:

- Owe less than $1,000 at filing

- Pay 90% of the current year's tax liability

- Pay 100% of the prior year's tax liability

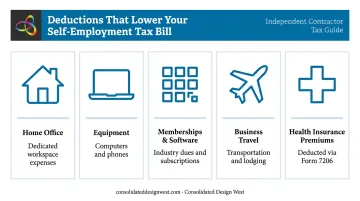

Common Deductible Expenses That Reduce Your 1099 Tax Bill

Reducing net profit reduces self-employment tax — which is why expense tracking matters all year, not just in April.

- Home office costs, provided the space is used regularly and exclusively for business

- Computers, phones, and other work-specific equipment

- Trade publications, software, and industry memberships

- Transportation and lodging for business travel

- Health insurance premiums (deductible for self-employed individuals via Form 7206)

For 1099 commission-only sales reps, including those working with Consolidated Design West, consistent expense tracking can noticeably cut the tax owed on commission income.

What If You Never Received a 1099 But Still Earned Income?

The IRS rule is clear: contractors must report all self-employment income regardless of whether a 1099 was issued — and missing this point is one of the most common (and costly) mistakes independent contractors make.

Per IRS Publication 525, income is taxable unless specifically excluded by law. Whether a form was issued is irrelevant. Cash payments, undocumented transactions, and sub-$600 payments are all reportable.

If you expected a 1099 and didn't receive one:

- Contact the payer to confirm it was sent

- If unresolved by late February, call the IRS at 800-829-1040

- Regardless, report the income based on your own payment records on Schedule C

The IRS can match bank deposits, compare records during an audit, and assess penalties — plus interest — on any income that goes unreported.

Frequently Asked Questions

Do I need to issue a 1099 to an independent contractor?

Yes — if you paid an independent contractor $600 or more in 2025 for services, and they are not a C corp, S corp, or paid via a third-party payment processor, you must issue Form 1099-NEC by January 31. For tax years after 2025, the threshold rises to $2,000.

Do independent contractors fill out a W-9 or a 1099?

Contractors fill out the W-9, which they provide to the hiring business. The business then uses that information to prepare and issue the 1099-NEC. The contractor does not complete their own 1099 — that's the payer's job.

Who is not required to receive a 1099-NEC?

Four main exemptions apply:

- Contractors operating as C corps or S corps (attorneys are an exception)

- Payments via credit card or third-party networks like PayPal (those trigger a 1099-K instead)

- Payments made for personal, non-business purposes

- Payments under the $600 reporting threshold

What happens if I don't receive a 1099 as a contractor?

You still must report all income earned. The IRS taxes income when earned, not when documented. Use your own payment records and report the accurate amount on Schedule C — the absence of a 1099 doesn't change your obligation.

What is the $600 threshold for a 1099?

If total payments to a contractor reach $600 or more in a calendar year, a 1099-NEC is required. Payments under that amount are still taxable to the contractor — they just don't trigger the business's filing obligation.

When is the deadline to send and file a 1099-NEC?

January 31 — for both sending Copy B to the contractor and filing Copy A with the IRS. Businesses filing 10 or more information returns must submit electronically through the IRS's IRIS or FIRE e-filing portals.